SEC Compliance Risk: Include it on your Current ESG Agenda

As asset owners increase their focus on environmental, social and governance (“ESG”) considerations within the investment process, and particularly climate-related considerations, asset managers are responding to these demands. However, while doing so they are unintentionally opening themselves up to compliance risk, with the U.S. Securities and Exchange Commission (“SEC”) increasingly scrutinizing asset manager ESG claims to protect investors, and flows of capital, from being subject to Greenwashing.

Clara Moreno Sanchez, Associate

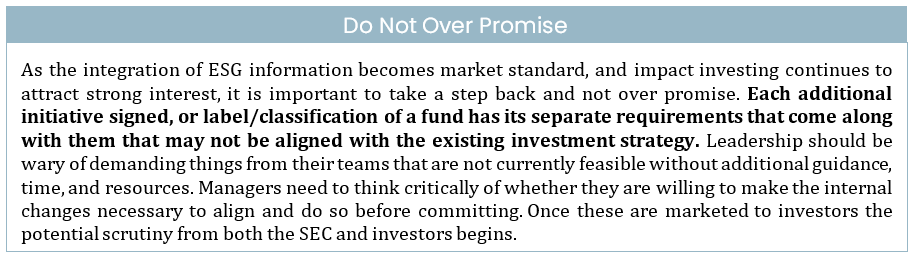

When managers rush to sign up to the UN supported PRI[1] and NZAM[2], state their intention to disclose funds under SFDR Article 8 or 9[3], or report in alignment with the TCFD[4], there is a tendency to overlook how these create a target for SEC examinations and potential to highlight deficiencies if not carried out with an appropriate compliance perspective. Given the SEC’s past cases and its 2023 examination priorities, ESG compliance risk should be on everyone’s current agenda, as the agency has been explicit in their intention to proceed with a significative enforcement of current regulations.

Headlines from past enforcement, including the latest charge against Goldman Sachs, have generated clear warning signs, but there seems to be confusion as to what the compliance risks are, and more importantly, how to mitigate them.

So, what are some common current ESG risks and how can one mitigate these?

The question is simply answered by looking at the purpose and principles that the SEC has always operated on. The SEC will act to enforce “the requirements that companies’ disclosures be accurate and not misleading, and that investment advisers adhere to their fiduciary duty and accurately describe their investment strategies” with regards to ESG (Gurbir S. Grewal, Director of the Division of Enforcement of the SEC). Grewal reiterates the point that these “are not new, and should be of surprise to no one.” [5]

To further eliminate this element of surprise, it’s helpful to specify what the SEC is actually evaluating. The SEC is not currently casting any moral judgements or assessing the quality of an ESG approach, but whether managers are truthful in terms of what they currently do, plan to do, and disclose all material information. As detailed below, firms can currently be put under SEC scrutiny through a wide array of reasons, which are worth exploring.

Misleading Statements

Many ESG-related cases revolve around investment managers and advisors making statements that have been deemed false or misleading by the SEC. Simply put, a misleading statement[6] is any statement that either contains untrue or incomplete information or presents information in a way that is likely to be deceiving to the consumer. The ruling not only applies to statements made in public filings or press releases, but also to statements such as oral claims made by company representatives to analysts or investors, marketing materials, social media posts, and Responsible Investment Policies.

This applies directly to statements on sustainability and ESG and is evidenced in the BNY Mellon case brought in 2022. BNY Mellon represented or implied in various statements that all investments in their funds had undergone an ESG quality review, even though that was not always the case. In its press release, Adam S. Aderton, Co-Chief of the SEC Enforcement Division’s Asset Management Unit confirmed that “the Commission will hold investment advisers accountable when they do not accurately describe their incorporation of ESG factors into their investment selection process.”

Violating this rule comes in many forms, whether it be by failing to disclose when the process deviates from the one disclosed, or including wording that may lead investors to an inaccurate conclusion.

Misleading by Omission

Under the current SEC rulings[7], filers need to disclose:

material information as defined by the federal securities law’s requirements; and

any information that make other statements made by the company materially accurate or not misleading.

As asset managers increase their disclosures to investors, it brings into scope the necessity to disclose additional information that may not have been explicitly required before. Once an ESG-related claim is made, any stipulations related to that claim need to be disclosed. Although the SEC is also working to formalize some required ESG and climate related disclosures[8], this ruling is already being used by the SEC for enforcement action on ESG disclosures that don’t contain all necessary information.

An example that brings this ruling to light is the SEC’s case against Fiat Chrysler in 2020 for failing to include information in their annual report on the limited scope of the internal audit conducted on the company’s vehicles’ compliance with environmental regulations. In this case, Fiat Chrysler disclosing they conducted an internal audit brought into scope the need for additional disclosure of all material information regarding the audit.

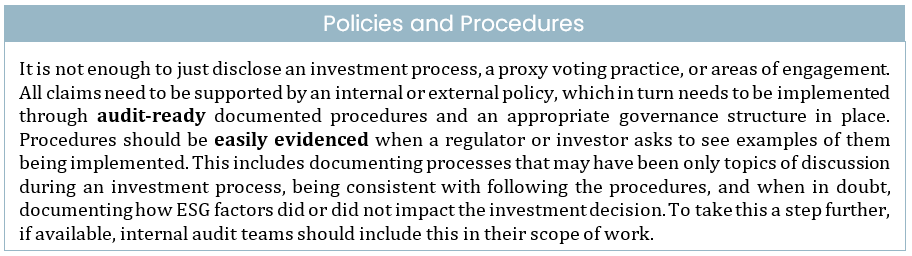

Policies and Procedures

An often overlooked but essential component of SEC compliance is the need to establish clear policies and procedures that ensure organizations are operating in accordance with securities laws. Under this rule[9], managers must create and implement guidelines and policies that are reasonably designed to ensure accuracy and completeness of disclosures, including those related to ESG.

Early in 2022, the SEC charged Wahed Invest, LLC, a robo-advisor, for misleading investors and not “[adopting] and [implementing] written policies and procedures reasonably designed to prevent the adviser from deviating from its claimed investment process” (Adam S. Aderton). A few month later in November 2022, Goldman Sachs was charged for both failing to have policies and procedures for one of their products and, once the policies and procedure were created, failing to implement them in their investment process. Findings included that ESG questionnaires were completed after securities were already selected for inclusion, which deviated from what was required in their policies and procedures.

This ruling can be applied to asset managers that claim alignment or compliance with an ESG or sustainability framework, code of regulation, such as TCFD, SFDR, and UN supported PRI, or simply publicly describing how ESG considerations are integrated into their investment process. Before any public disclosure of any activity, managers need to have documented and formalized internal processes to ensure adherence to it.

Fraud

More obviously, outright false statements on an investment process, metrics, or other disclosures will undoubtedly be scrutinized by the SEC. Usually, these cases require the proof of intentionally in making deceptive statements, the manipulation of information, or omission of information. Greenwashing is a hot topic in the market, and managers should operate with the assumption that any number or statement disclosed to the public can be examined.

Include SEC Compliance Risk on your ESG Agenda

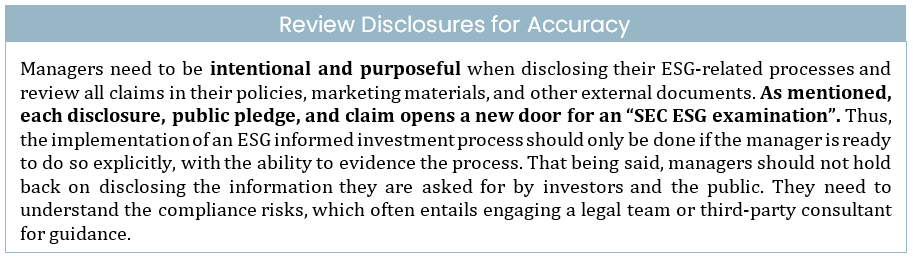

As managers focus on aligning with investors’ needs and feel the need to ‘catch up’ on ESG, it is natural to delay the review of marketing materials, spend time evidencing their investment processes, and including detailed information on disclosures. But, as we see these risks materialize, our main recommendation is this: Include SEC compliance risk on your ESG agenda.

How NorthPeak Advisory Can Help

[1] The United Nations support Principles for Responsible Investment (PRI) is a global network of investors working to promote sustainable and responsible investment practices. There has been a significant increase in Investment Manager signatories of the PRI, with a 70% increase in U.S. headquartered managers since the end of 2020.

[2] The Net Zero Asset Managers initiative is an international group of asset managers committed to supporting the goal of net zero greenhouse gas emissions by 2050 or sooner.

[3] The Sustainable Finance Disclosure Regulation (SFDR) is a European regulation that aims to improve transparency and disclosure of sustainability risks in financial markets and products.

[4] The Task Force on Climate-related Financial Disclosures (TCFD) is a global initiative that provides voluntary recommendations to help companies and organizations disclose climate-related risks and opportunities.

[5] 2021 Scott Friestad Memorial Keynote Address

[6] Rule 206(4)-1 under the Investment Advisers Act of 1940

[7] Rule 206(4)-8 under the Investment Advisers Act of 1940

[8] In October of 2023, the SEC plans to announce rulings related to fund name requirements, the categorization of ESG fund-type, disclosures of proxy voting and engagement as part of fund’s strategies, and for some ESG-focused funds, disclosure of their carbon footprint and carbon intensity of their portfolios.

[9] Rule 206(4)-7 under the Investment Advisers Act of 1940